In fact, some commentators are suggesting that the value premium no longer works. Many investors have abandoned it altogether. So would it be sensible or foolhardy to join them?

First, some perspective

There is certainly no reason for value investors to despair, especially those with globally diversified portfolios. Value has held up rather better in markets outside the US.

Another point to make is that most of the outperformance of growth over value has occurred in the last three years. Between 2010 and 2016, returns from growth and value stocks were very similar.

Why has value underperformed?

Nevertheless, there is no denying that value has lagged the broader market, and it begs the question, Why?

Arnott, Harvey, Kalesnik and Linnainmaa examined the cause of value’s underperformance in their December 2019 study, Reports of Value’s Death May Be Greatly Exaggerated.

They compared the period before the global financial crisis of 2007 with the period that followed it, and discovered that the relative profitability of value and growth stocks had remained fairly constant.

Nor had there been any significant increase in what’s known as migration. This occurs when value stocks become more valuable and migrate from the value portfolio to either neutral or growth, or when growth or neutral stocks become cheaper and drop into the value portfolio. Migration is a major contributor to the relative performance of value to growth.

Their findings led Arnott et al. to deduce that the simple explanation for value’s underperformance is the relative increase in the valuations of growth stocks. And while valuation spreads are not perfect predictors of the future, several studies have shown that they are the best predictors of future returns.

The authors concluded:

Unless we choose to assume that the valuation spread between value and growth stocks will continue to widen indefinitely, value seems poised to outperform growth, perhaps by a startling margin.

Has value become overcrowded?

The research conducted by Arnott et al. also puts to rest another common theory about the value factor. Some have argued that value funds have become too popular, and that this ‘overcrowding’ has effectively neutralised the value premium.

But the dramatic widening of valuation spreads highlighted in the research is the opposite of what you’d expect if there were overcrowding. If anything, it seems to reflect herding into stocks with high growth opportunities.

This is not to say that growth stocks will not deliver higher profits compared to value stocks in the future; they almost surely will. However, they are priced at a level that reflects that and then some. History shows that returns can revert to the long-term mean within a very short period.

We’ve been here before

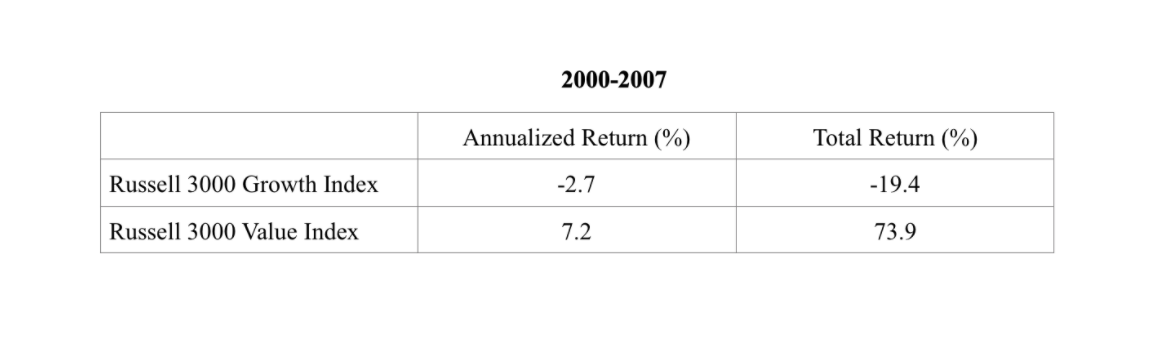

In fact you don’t need to look too far back in history for an example. From the start of 1998 to the end of 1999, the Russell 3000 Growth Index outperformed the Russell 3000 Value Index by a massive 59.6%. Value was dead, some declared; we had entered a new era.

What happened next? The growth bubble burst in March 2000 and, as this table shows, value trounced growth over the next few years.

Source: Dimensional Fund Advisors

Indeed, it wasn’t until 2017 that growth began to outperform in earnest. Between 2000 and 2016 the Russell 3000 Value Index outperformed the Russell 3000 Index by 147.2% in terms of total return.

Recency effect

What we saw in 1999 and what we’re seeing again now are classic examples of recency bias.

This is the tendency to overweight recent events and trends and ignore long-term evidence. It leads investors to buy after periods of strong performance, when valuations are higher and expected returns are now lower, and sell after periods of poor performance, when prices are lower and expected returns are higher.

Buying high and selling low is a surefire way of underperforming. Disciplined investors do just the opposite, having the courage of their convictions to sit tight, rebalancing periodically to maintain their original asset allocation.

Simple but not easy

This prescription for successful investing may be simple, but that doesn’t mean it’s easy.

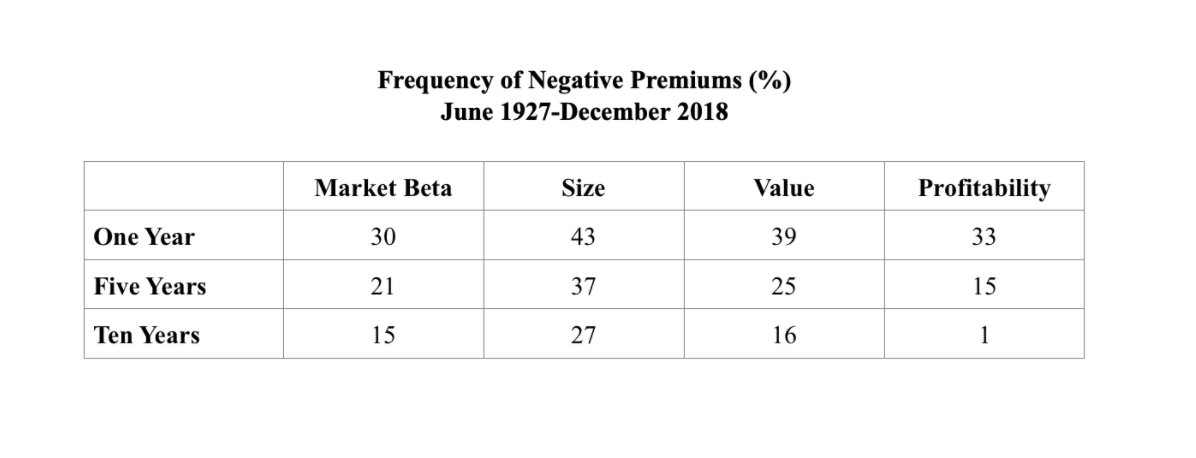

Look at the chart below, for example. It shows the performance of US stocks generally, and of three major risk factors in particular (size, value and profitability), between 1927 and the end of 2018.

Source: Dimensional Fund Advisors

As you can see, all four premiums experienced long periods of underperformance. Even at ten years, the equity premium was negative 15% of the time — only slightly less than the value premium at 16%.

The key takeaway here is that when it comes to equities, ten years can be nothing more than noise, and certainly isn’t a reason to abandon your chosen strategy.

The good news

The bad news, then, is that the market as whole, and different segments of it, will inevitably underperform for long periods. The good news is that, through diversification, you can smooth those periods out.

In their March 2020 paper Is (Systematic) Value Investing Dead?, Israel, Laursen and Richardson concluded that “the diversification benefit of value strategies cannot be overstated”:

Value strategies are typically not utilised on a stand-alone basis. Investors tend to incorporate value measures with other well-known strategies. Given that each of these investment themes work well individually, and each of the themes are lowly, or negatively correlated, a risk-balanced combination across themes is a powerful diversifier.

A question of probabilities

There are no guarantees in equity investing. It’s by no means certain that value stocks will produce long-term outperformance in the future.

But successful investing is all about putting the odds in your favour. On average, since 1927, value has provided a premium in the region of 4% a year.

True, the recent picture looks very different, but the probability is that the value premium is not dead but dormant. Who knows? It may rise from its slumbers sooner than you think.

Robin Powell is editor of The Evidence-Based Investor. You can follow him on Twitter @RobinJPowell.